For more than a year, the whole world has been living with COVID-19 and related restrictions. The coronacrisis had a huge impact on the transport and logistics industry represented by sea, rail and air cargo transportation. Some of them continue to be in crisis mode, while others have become beneficiaries of the crisis.

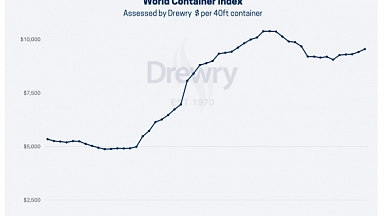

Sea cargo transportation in the direction of China-Europe-China has been in a state of crisis since the beginning of the pandemic. If in April 2020 the rate of the WCI Drewry index reflecting the cost of sea freight between East Asia and Europe was USD 1,495 per FEU, then in April 2021 it was already USD 5,472 (+266%) with an upward trend.

Maritime cargo transportation faced disruptions in global value chains, which exacerbated structural market imbalances and led to a cluster of containers in North America and Europe, as well as a sharp increase in transportation rates.

In air transportation in April 2020, a historic drop in volumes was recorded, thereby amounting to more than 90% compared to year-on-year. If we talk about numbers, in the past 2020, the pandemic caused damage to the air transportation industry of the order of USD 370 billion of lost income compared to 2019. Although the situation is improving, according to a number of forecasts, the market will not recover to previous levels until the end of 2022.

The beneficiary of the coronacrisis was railway container transportation in the direction of China-Europe-China. If in 2019 333,000 TEU were transported along the Eurasian railway route, then in 2020 this figure has increased already to 546,900 TEU, and in the first half of 2021 it was 352,700 tons, which is more than the indicator for the whole of 2019.

Against the background of the pandemic, the railway has proved to be a reliable, predictable mode of transport. The railway was much less susceptible to coronavirus restrictions, and the rate for rail freight remained stable in the range of USD 2,600-2,700 per FEU.

Nevertheless, mass vaccination and the recovery of transport logistics from the crisis state put on the agenda the issue of the sustainability of restoring air cargo transportation, the speed of returning to the normal level of sea freight rates, and preserving the advantages of the railway in the long term. What will be the transport logistics after the pandemic?