A slight easing in major global ocean freight markets and prices since China’s early October Golden Week holiday has continued this week, especially on the transpacific, with prices stable on the main trades, including ex-Asia, according to the latest figures from Freightos and Drewry.

But despite easing rates with anecdotal reports that some shipments can be booked as little as one week in advance without paying a premium, the lull is likely to be short-lived ahead of early bookings for Lunar New Year, digital freight pricing and management specialist Freightos believes.

Judah Levine, head of research at Freightos, noted that despite continued delays at the ports of LA and Long Beach, skepticism that the White House push to keep truck gates open 24/7 will drive improvement in the near term, and congestion spreading to other ports, «there are indications that Asia-US ocean demand is easing, at least a little».

In addition to Asia-US West Coast rates going unchanged this week and remaining 16% lower than their mid-September peak, he said logistics providers on the Freightos.com marketplace «are seeing other signs of a let up».

Fewer booking premiums

For example, Robert Khachatryan, CEO of the company Freight Right, reports that for the first time since June some transpac space can not only be booked without premium guarantees, but also is «available as little as one week in advance.» Khachatryan attributes part of the dip to the delays, with shippers still waiting for containers en route holding off or cancelling any additional shipments.

And according to Miranda Qin of Seabay Logistics, another forwarder available on freightos.com, both suppliers and importers say that supply constraints from the recent energy shortages in China — driven by rising coal costs and efforts to reduce emissions, which are expected to continue until the spring — are also contributing to a dip in demand, Levine highlighted.

But he said there had been «no comparable rates dip on the Asia-Europe lane, where importers are equally exposed to production slowdowns in China and are also dealing with port congestion challenges. So, the easing on the transpacific — with longer transit times and delays than to Europe and 25 December rapidly approaching — likely also indicates a let up in the underlying holiday-driven demand.»

Levine continued: «If this is the start of a minor lull, it is likely to be short-lived. Just as retailers pulled peak season orders earlier than usual to account for delays, so too the other ocean freight peak around Lunar New Year (which begins 1 February 1st) is likely to start early.»

Air cargo rates extremely elevated

In the meantime, ocean delays are helping to keep air cargo rates extremely elevated. The Freightos Air Index (FAX) composite global index is at $6.80/kg, 22% higher than at the start of the year, with Asia-US West Coast rates at $12.70/kg, a 40% climb since the end of August.

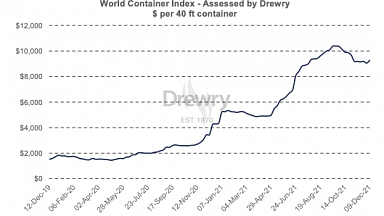

Drewry’s latest World Container Index report today indicated that the composite index of the e-ght east-west major trade lanes measured combined, decreased 0.4% this week, but at $9,865.14 per 40ft container it remains 281% higher than a year ago. The average composite index of the WCI, assessed by Drewry for year-to-date, is $7,191 per 40ft container, which is $4,661 higher than the five-year average of $2,530 per 40ft container.

Freight rates on New York — Rotterdam gained 3% or $35 to reach $1,189 and rates from Los Angeles — Shanghai grew 1% to reach $1,315 per 40ft box.

But otherwise, spot prices were flat or slightly declined. Rates on Shanghai to New York, Rotterdam to New York, Rotterdam to Shanghai and Shanghai to Genoa declined 1% respectively per 40ft container. Rates on Shanghai- Rotterdam and Shanghai-Los Angeles hovered around the previous week’s level.

Drewry expects rates to remain steady in the coming week.

Dips in demand

Freight forwarder Flexport’s latest Ocean Freight Market Update this week noted that the Asia to North America (TPEB) trade saw premium and extra loader market prices soften «due to dips in demand for the most expensive space on TPEB».

Flexport added: «Whether rates will continue to flatten, further reduce, or even increase remains unclear. Carriers have indicated that the demand outlook remains strong through the end of the year. This is in line with projections by economists, indicating strong forecasts until inventories replenish. Congestion is expected to remain severe.»

It noted that carriers had «extended or even reduced rates as of 2H (second half of) October», but highlighted that «rate levels remain elevated», while space and availability of containers remained «critical», with «severe undercapacity», recommending that customers «continue to book well in advance — at least 4 to 6 weeks from CRD (cargo ready date) to target ETD for best chance of hitting timelines.»

For Asia to Europe (FEWB), «space and equipment crunches continue. Market demand is consistently exceeding supply, and rates have been very high for a long period», Flexport said.

It noted that the overall space situation was still being worsened by blank sailings and poor equipment availability, noting: «Carriers are overcommitted and are limiting booking acceptance or rolling shipments. With continuous vessel delays and shifts, schedule reliability is very low. Power shortages are affecting factory production up to a certain extent and causing more changes in shipping plans.

«Rates remain at a record high level, but have been reasonably stable throughout October. Most carriers have extended their premium rates.»

US terminal congestion

On Europe to North America (TAWB), Flexport noted that «terminal congestion along the US East Coast is now impacting vessel schedules with some lines cancelling Savannah calls and replacing them with Charleston or Jacksonville. Congestion at LAX/LGB is also causing lines to now omit both ports and impacting schedules.»

On TAWB pricing, Flexport said GRI rate rises for 1 October had been implemented, predicting «rates will stay strong for all Q4 2021».

And for Indian Subcontinent to North America, Flexport said forward-looking rates were softening, although «strong demand, equipment deficits, and port omissions continue to challenge the Indian Subcontinent». But rates had softened, with no expected increases through end of October.