Staple three-month deals with forwarders and NVOCCs were all but suspended last year as carriers carefully choose the counter-parties they wanted for their long-term contracts of 12 months or more, with the remainder of shippers consigned to the spot market or, at best, offered rates valid for a month or less.

But according to the Ningbo Containerized Freight Index (NCFI) commentary, there was «insufficient demand» this week for loaders from China, prompting carriers to either blank sailings or start discounting rates.

A UK-based forwarder with an office in China told The Loadstar carriers were «starting to show more interest» in his business, adding: «I was quite surprised to receive a call this week from one of our liner company contacts suggesting a meeting.

«He’s been hiding from us for the last few months and suddenly he wants to talk, so it must mean they are looking for cargo again.»

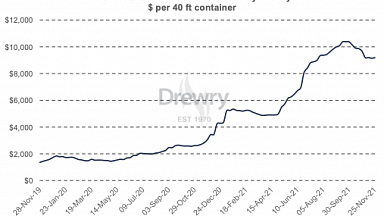

All the Asia-North Europe indices reflect the softening of demand, the biggest fall on Drewry’s WCI index, which slumped another 8% this week, shedding over $1,000 and taking the spot rate back down to $11,192 per 40ft. This component has lost nearly $3,000 since its peak before Chinese New Year.

But before shippers get carried away with thoughts that rates on the route will totally collapse, there is a further cautionary note from Vespucci Maritime’s Lars Jensen. He argues that the 20% fall in rates is, in fact, below the average 29% decline seen in the past eight years during slack season weeks following CNY.

Moreover, the spot rate decline may be short-lived if the lockdown disruptions in China begin to ease, allowing a more regular flow of exports onto the terminals.

Meanwhile, on the transpacific, there was a slight softening this week in spot rates from Asia to the US west and east coasts, with the Freightos Baltic Index (FBX) settling at $15,908 and $17,318 per 40ft, respectively.

«While the temporary dip in available supply of exports could explain the slight easing, all signs point to continued elevated volumes and rates in the coming months,» said Judah Levine, head of research at Freightos.

However, Jon Monroe, of Washington state-based Jon Monroe Consulting, reports that the eagerly anticipated carrier negotiations with NVOCCs are «not as hot and heavy as expected». This suggests a slight shift in the sentiment on rates for the tradelane.

«Many NVOCCs are now taking a ‘wait and see’ attitude to their negotiations,» said Mr Monroe.

He also reported on reprisals by carriers against shippers chartering or using their own tonnage to overcome supply chain disruptions — a detestable tactic also used by a few carriers in North Europe, according to reports to The Loadstar.

«Some ocean carriers have even threatened companies that chartered vessels by refusing to grant contracts to them,» said Mr Monroe.