When using, citing, or distributing the materials from this report, it is mandatory to reference the ERAI portal and include the webpage address https://index1520.com as the source of information.

China-Europe logistics market

Demand outlook

- In September, Chinese manufacturing enterprises significantly increased their procurement of raw materials and components [S&P Global]. This trend may signal an acceleration in industrial production and a strengthening of the country’s export potential. Key regions driving demand growth include South America, Southeast Asia, and Africa (including potential re-exports to the US). Meanwhile, no significant demand fluctuations have been recorded from Europe.

- In September, export conditions for German industry improved again, with the HCOB Export Conditions Index reaching 51.3 [S&P Global]. New export order volumes stabilized, supported by demand from Asia and North America. The strongest performance remains in the mechanical engineering and consumer goods sectors, while the chemical and automotive industries continue to contract.

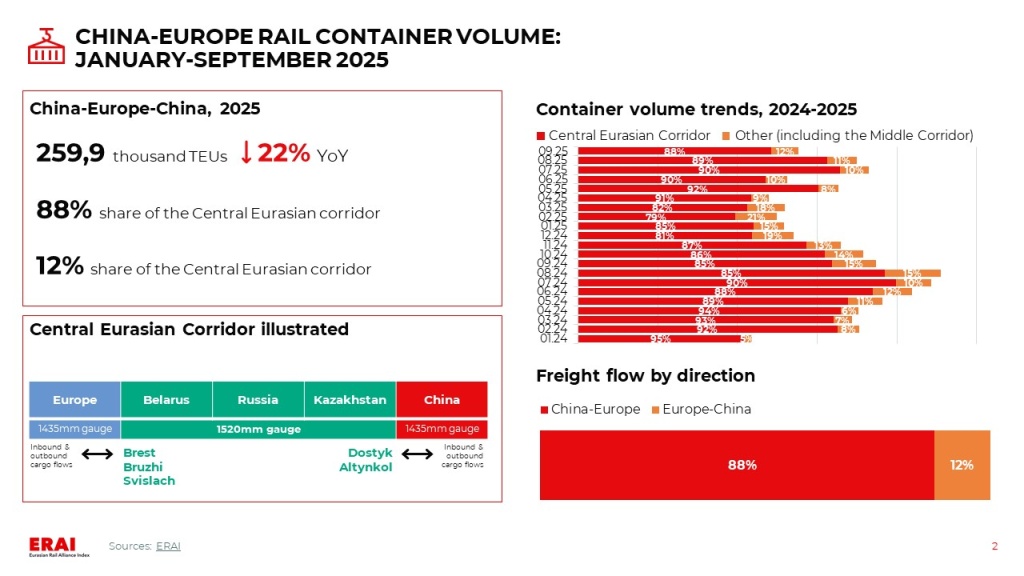

- For January—September, China—Europe—China rail container volumes fell by 22% YoY. In September, total volume across all competitive routes declined by 23% YoY and 18% MoM. This sequential decrease was primarily driven by a contraction in the central Eurasian corridor. The Middle Corridor also registered a volume decrease of approximately 8% MoM.

- Contrary to earlier forecasts, demand for Asia-Europe sea freight began to rebound after the Golden Week holiday, although the pace of recovery remains subdued.

Freight rate trends

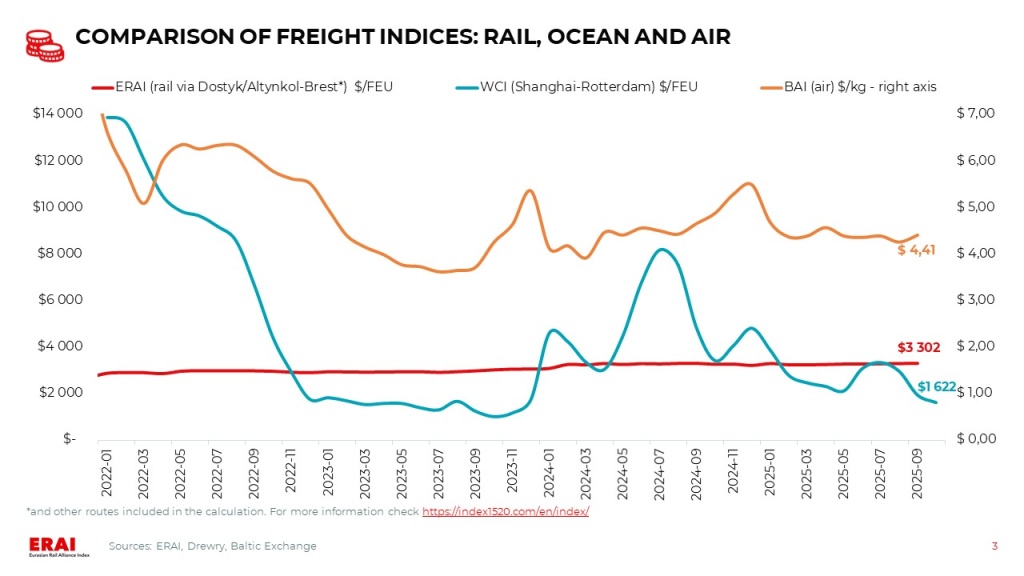

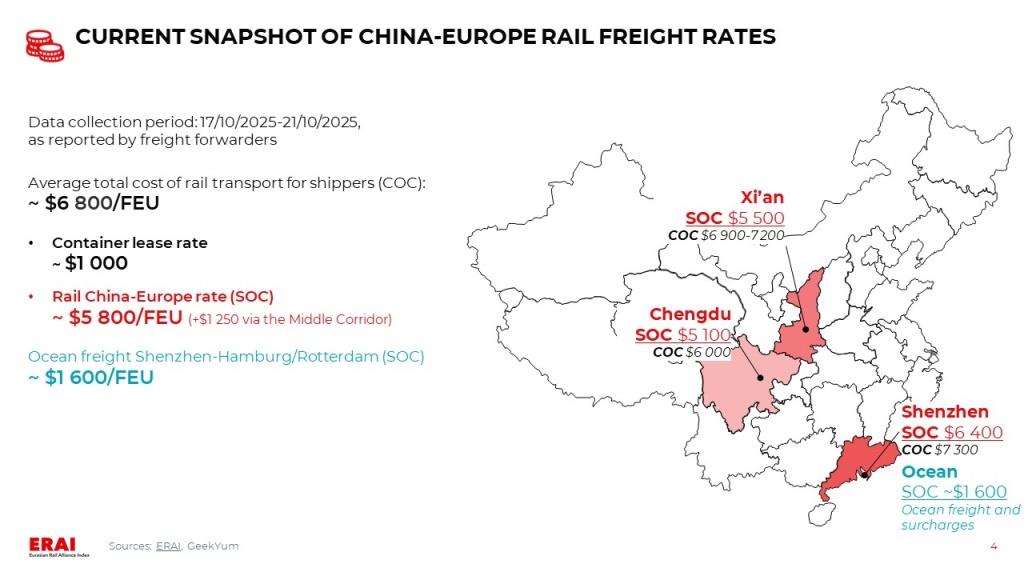

- The average China—Europe rail shipping rate for late October shipments is approximately $5 800 per FEU (SOC). Rates vary by origin, ranging from ~$5 100/FEU (Chengdu) to ~$6 400/FEU (Shenzhen). Container lease rates range from $800 to $1 100.

- The WCI Shanghai—Rotterdam increased by 6% over the past week to $1 669/FEU (-13% MoM, −51% YoY) [Drewry]. This marks the first time the index has halted its decline since late July. Carriers have raised FAK rates for the second half of October and have officially announced a General Rate Increase (GRI) for November [Flexport]. Port congestion, potential blank sailings, and the risk of equipment shortages in early November increase the likelihood of these measures holding. According to GeekYum, the average rate from major carriers is ~$1 900/FEU for the remainder of October and ~$2 600/FEU for the first ten days of November.

- Futures pricing points to a moderate increase in ocean freight rates through the end of 2025. Specifically, Asia—Europe rates are projected to gradually rise to approximately $2 300 per FEU by the end of this year.

UPDATE: As of the evening of October 23, 2025, the latest WCI Shanghai-Rotterdam reading has risen by 4% WoW — up to $1 736/FEU.

Other trends

- Following a successful pilot voyage along the Northern Sea Route (NSR), operator Sea Legend Shipping has announced plans to launch a regular service starting in the summer of 2026 (1-2 sailings per week) [Global Times]. During the non-navigable season, the company plans to implement a multimodal solution: sea delivery via the Suez Canal, followed by a rail leg to terminals in Europe (total transit time is approximately 25 days). This service will serve as an alternative to the China-Europe Railway Express. In the future, the company aims to transition to year-round navigation via the NSR.

- On October 15, 2025, a new China-Europe Railway Express route was launched on the Wuhan—Northern Europe corridor [HUBEI.GOV; Fuootech]. Upon arrival in Hamburg, a portion of the cargo will be redirected via three multimodal routes to the ports of Esbjerg (Denmark), Gothenburg (Sweden), and major Norwegian ports. The transit time will be approximately 22 days.

|

|

|

Ocean freight: short-term market uplift post-holiday, amplified by European port disruptions

Current Situation and Near-Term Outlook: a modest demand uptick and European logistical disruptions are laying the groundwork for a reversal in freight pricing.

- Contrary to earlier forecasts, demand for Asia-Europe sea freight began to rebound after the Golden Week holiday, although the pace of recovery remains subdued.

- While conditions at Asian ports have stabilised, significant operational disruptions persist in Northern Europe. Strikes in Benelux ports have caused terminal congestion, and despite the rather quick end of the protests, it will take several weeks to clear the backlog. With ongoing sysyemic container pick-up restrictions, these disruptions are further destabilising European supply chains. As of 19 October 2025, port delays amounted to 504 thousand TEUs in Northern Europe (up 106% MoM) and 738 thousand TEUs in Northern Asia (down 54% MoM) [Linerlytica].

- The WCI Shanghai—Rotterdam increased by 6% over the past week to $1 669/FEU (-13% MoM, −51% YoY) [Drewry]. This marks the first time the index has halted its decline since late July. Carriers have raised FAK rates for the second half of October and have officially announced a General Rate Increase (GRI) for November [Flexport]. Port congestion, potential blank sailings, and the risk of equipment shortages in early November increase the likelihood of these measures holding. According to GeekYum, the average rate from major carriers is ~$1 900/FEU for the remainder of October and ~$2 600/FEU for the first ten days of November.

- Despite a declared ceasefire in Gaza and initial announcements about service resumption, most carriers are maintaining a wait-and-see approach. A full resumption of Suez Canal transit is considered contingent on several months of sustained regional stability, according to HSBC estimates [JOC].

UPDATE: As of the evening of October 23, 2025, the latest WCI Shanghai-Rotterdam reading has risen by 4% WoW — up to $1 736/FEU.

Mid-and Long-Term Outlook: the overall trend, as before, points to a growing imbalance between supply and demand and intensifying competition among carriers.

- Shippers are now negotiating medium- and long-term contracts in a market characterised by intense carrier competition. This dynamic is evident in recently signed medium-term contracts, where freight rates are running approximately 56% below prior-year levels [JOC]. Beyond steep price concessions, Drewry notes that shippers can secure improved terms, such as extended payment deadlines and binding service-level agreements.

China-EAEU logistics market

Import and export trends

- Bank of Russia analysts have revised the macroeconomic forecast for 2025 downward: inflation is expected to reach 6.6%, while GDP growth will slow to 1%. The key rate is projected to average 19.2%. According to Rosstat, consumer prices in September 2025 increased by 0,34% MoM and 7,98% YoY. The rates were higher than in August (0,26% MoM, 7,5% YoY), and annual inflation stabilized near the lower boundary of the Central Bank’s forecast range of 8–8.5%.

- Consumer demand continues to show steady growth: nominal expenditures in September increased by 11% YoY, with retail turnover growing by 10%. The main drivers were rising incomes and a revival in credit activity. A short-term surge in demand is possible in 4Q2025 due to the anticipated VAT increase; however, a normalization of the trend is likely in the medium term [Kommersant]. The current resilience of demand supports the volume of consumer goods imports, but an expected slowdown in consumption growth in 2026 will restrain imports.

- The Bank of Russia will consider the possibility of adjusting the key rate on October 24. Despite remaining room for easing, the decision will be made considering the pace of inflation deceleration and the upcoming VAT hike, which complicates achieving the 4% target. Most analysts expect the rate to be maintained at the current level or a symbolic reduction of 0,25-0,5%, with further monetary policy easing likely only in December 2025 [Kommersant].

- According to the IPEM forecast, railway container transportation in 2025 will decrease by 4,8% due to the steady shift of shippers to road transport. Additional pressure on the market will come from the VAT increase and tight monetary policy [PortNews].

- In addition to the «ship-or-pay» principle, the Ministry of Transport of Russia proposes amendments to the Railway Transport Charter requiring shippers to coordinate transportation requests with wagon operators. Experts note that the measure will improve transportation planning quality, but it has been met with mixed reactions in the operator community. Critics fear increased shipper dependence on operators and a potential shift of cargo to road transport [1520international].

- In September 2025, the total container throughput of Russian seaports decreased by 10% YoY, amounting to 408.6 thousand TEU. The sharpest decline was in imports (-16%), while exports decreased by 8% [InfraNews].

- The return of the French container line CMA CGM to the Russian market has reignited discussions about the need to protect domestic carriers. The first container ship is scheduled to arrive at the port of St. Petersburg on November 17, with subsequent weekly calls [Kommersant]. CMA CGM’s return will intensify tariff pressure on the market, creating additional challenges for Russian carriers amid declining imports. No overall market volume growth is expected—only a redistribution of existing cargo flows will occur.

- Import rates in the China-Moscow multimodal corridor continue to remain stably low; however, a slight increase has been noticeable over the past 2 weeks (+$200/FEU), with the average transportation cost via Far Eastern ports at ~$4 150/FEU (SOC). In contrast, rates for direct rail transportation have decreased by $200/FEU and stand at ~$4 800/FEU (COC).