The European Union is China’s largest trading partner. China is the EU’s second largest trading partner after the United States, but it is catching up rapidly. The sustained growth of the Chinese economy and its integration into global supply chains have put China on a path to become the world’s largest trader and its largest economy, measured at market exchange rates. When measuring by purchasing power parity, it is already the world’s largest economy.

Since 2000, China’s real GDP has multiplied almost fivefold, while the EU’s grew by 20% and the United States’ by 41%. Over this period, Chinese growth has averaged 9%and has consistently stayed above 6%. At the beginning of the catch-up process, China had a very low level of development. Even today, per capita income in China amounts to only about one quarter of EU per-capita income at market exchange rates.

China’s exports have grown even faster than the rest of the economy, especially before the global financial crisis, though the rate of growth has slowed in recent years. China’s share of world export markets surged from 3% in 2000 to around 11%in 2015, and has since stabilised.

Since China joined the World Trade Organisation in December 2001, the EU’s goods exports to China have grown on average by more than 10% a year, and its services exports by more than 15% a year. This has generated ample benefits for EU producers and consumers. However, as imports from China have also grown rapidly, it has also caused some degree of disruption to EU labour and product markets.

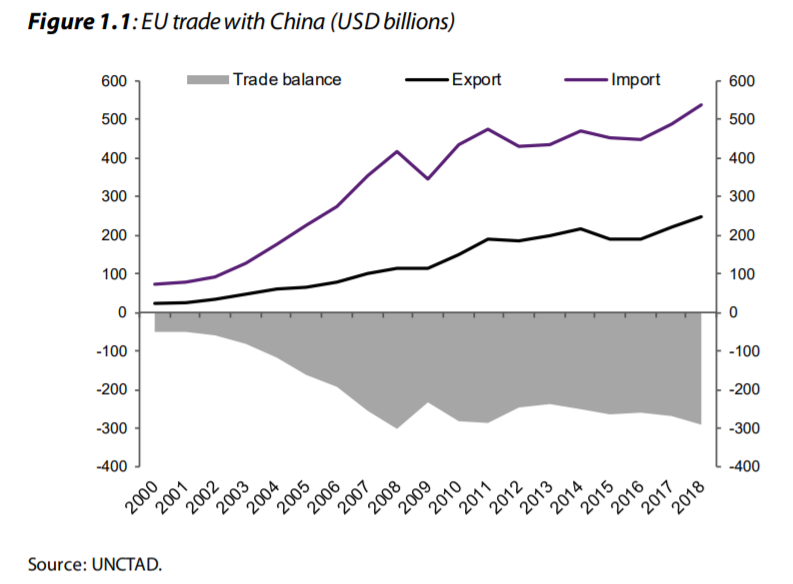

Currently, China is the second largest market after the US for EU exports, but EU exports to China have been outpaced by China’s exports to the EU. The EU’s trade deficit with China has grown to USD220billion.

The EU’s trade deficit with China is significantly lower than the US trade deficit with China, but it is still important to note that the EU deficit with China is larger thanthat reported by Eurostat. Comtrade statistics which offer more accurate bilateral balance information between EU member states and China show that the bilateral balances between individual EU countries and China are lower than the Eurostat data suggest.

According to Comtrade, Germany runs a USD16billion trade deficit with China, while the Eurostat data show a surplus for Germany.

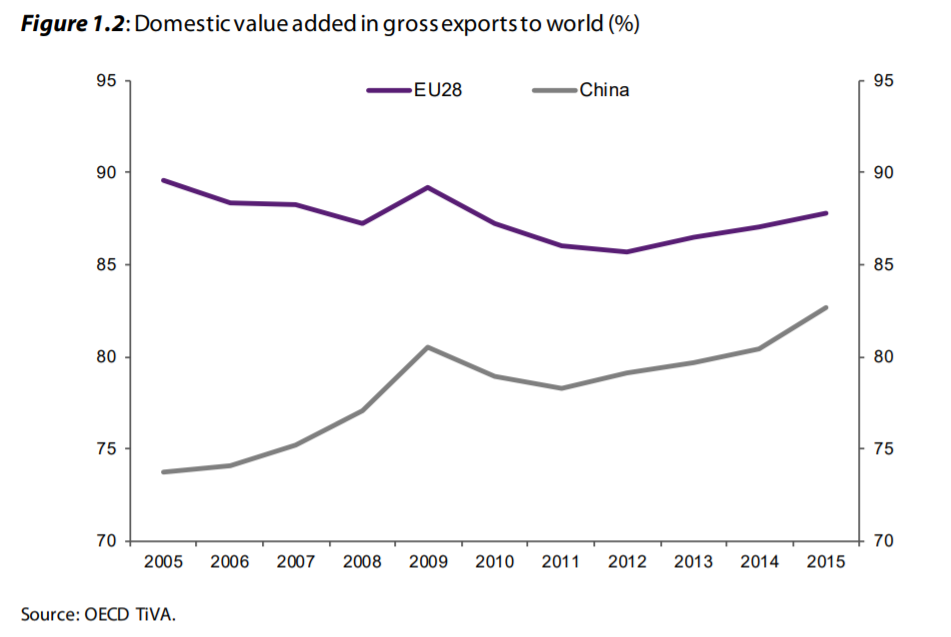

The difference in terms of value added between EU exports to China (relatively high) and Chinese exports to EU countries (relatively low) was so large that running a bilateral trade deficit in gross terms would overestimate the situation, compared to the actual trade deficit in value added terms. More recently, however, this has been less the case as China has moved up the ladder and the value-added component of exports has increased.

China has become much more important in the global supply chain. This has multiple implications for the EU-China trade relationship and the global economy more broadly. When it comes to the globaleconomy, the coronavirus outbreak is an important reminder of just how central China has become to global value chains. The shutdown of parts of China, especially Hubei province, has resulted in significant disturbances to global supply chains. The changing nature of China’s supply chains and China’s ascent of global value chains also affects EU member states’ integration with each other in terms of trade in intermediate goods. In fact, while the size of the intra-EU value chain has shrunk (countries are more loosely bound to each other in their exports of intermediate goods), EU member states have become increasingly linked to China for intermediate goods.

When China joined the WTO in December 2001, it benefitted from a reduction in the tariffs faced by its exporters, as other WTO members were required to adopt the most-favoured nation principle for China. Moreover, uncertainty about trade policy declined significantly. The WTO provides members with tools to protect themselves from unfair competition. In 2018, roughly half of the trade-defence instruments used by the EU were applied to China. In particular, anti-dumping measures were widely used and have been shown to effectively dampen trade. Their use increased significantly from the beginning of China’s WTO membership until 2006; since then the number of new cases has declined. In 2019, the EU initiated only two anti-dumping cases against China, out of a total of five anti-dumping cases initiated by the EU. China has initiated far fewer cases against the EU, with fewer than two new cases per year since WTO accession.

The ratio between EU and Chinese cases also reflects the trade balance between the two economies. Finally, other countries have more frequently used anti-dumping instruments against China than the EU. In particular, India, the US and Brazil have been among the most frequent users of anti-dumping measures against China. Globally, more than 600 anti-dumping measures are in force against China, with only a fraction coming from the EU. Finally, the EU’s anti-dumping measures are particularly important in base metals and the chemicals and pharmaceutical sectors (Felbermayr and Sandkamp, 2020).

In December 2017, the EU adjusted its trade-defence rules, particularly its methodology for calculating dumping margins. This is of particular relevance for the EU’s trade policy stance towards China, because the EU has removed the specific provisions governing the calculation of anti-dumping duties for China and other non-market economies. Under the old rules, China was the largest target of EU anti-dumping duties and was also subject to higher duties than Europe’s other trading partners. The change in rule de facto shifted the burden of proof from Chinese firms to the European Commission. It is now the Commission that must prove export prices are distorted for non-market economy reasons. In cases since 2017, the Commission seems to have consistently argued that prices are distorted. The new methodology has also allowed higher duties to be applied. European anti-dumping legislation reform might not significantly change how China is treated in EU anti-dumping investigations.However, it certainly requires the EU to be more transparent and to carefully explain on a case-by-case basis why Chinese exporters are treated differently from those of other countries.

On 14 February 2020, the US-China Economic and Trade Agreement (ETA) entered into force. It may mark a turning point in the Sino-American trade war, which saw US tariffs against China increase from an average of 3.8 % at the beginning of 2018 to 21 % in the summer of 2019 (Bown, 2020). The ETA does not address tariffs at all (ETA, 2020). However, the agreement commits China to increasing its imports from the US. These targets will be difficult to meet, not least because of the growth slow-down resulting from the coronavirus crisis. Chowdhry and Felbermayr (2020) estimated how the envisaged increase in Chinese imports from the US might affect EU exports to China.

In 2021, China would import goods worth USD193.3 billion from the US under the ETA scenario, compared to USD 130.7 billion under the no-ETA scenario. This would be an increase of 48%, attributable to the ETA. Mechanically, imports from the EU would decline by USD 10.8 billion (from USD 202 billion to USD 191.2 billion), equal to 5 % of the undistorted benchmark. The EU’s manufacturing sector, particularly aircraft and vehicles, would be hit hardest. In addition, the China-US ETA could make it difficult for China to honour its commitments to the EU regarding the protection of Geographical Indications. The EU could, however, benefit from the ETA’s provisions reducing restrictions on foreign equity in China and its aim to strengthen intellectual property protection.

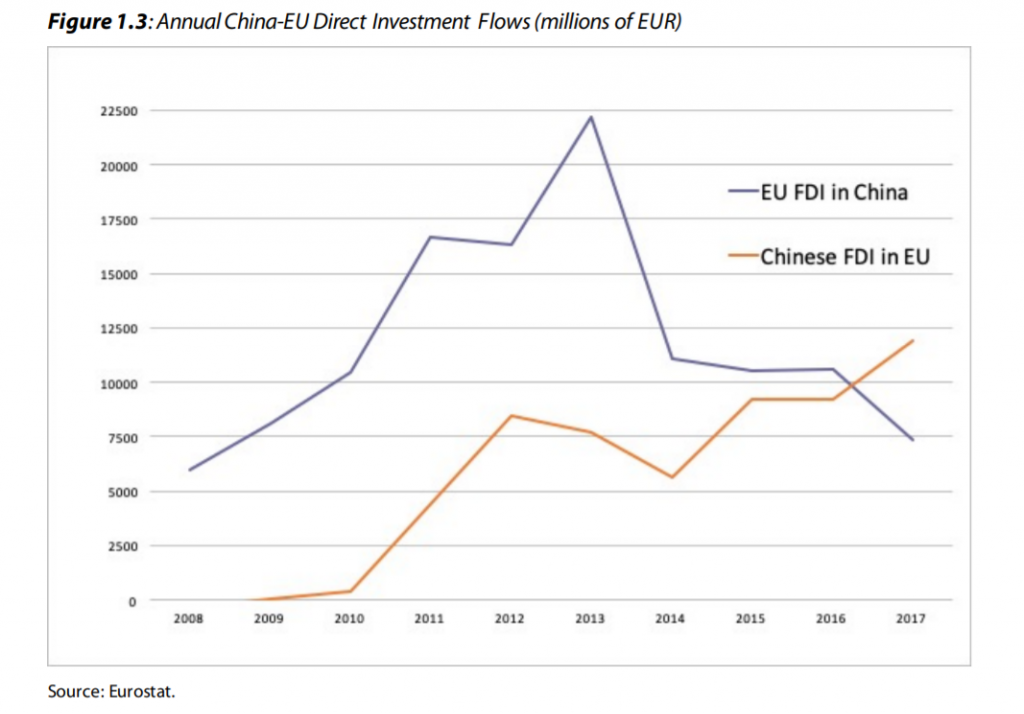

Foreign direct investment (FDI) flows between the EU and China are substantial but their stock is underdeveloped compared to the sizes of the two economies (Dadush et al, 2019). While FDI has increased as trade between the EU and China has surged, bilateral FDI flows remain small in relation to the size of both economies, and have been relatively volatile.

Nevertheless, from 2008 to 2017, the stock of EU FDI in China grew from EUR 54 billion to EUR 178 billion — an increase of 225 %. Meanwhile, the stock of Chinese FDI in the EU rose nearly tenfold, reaching EUR 59 billion in 2017. The rise of Chinese FDI should be no surprise, given China’s emergence as an important economic power with a declining domestic rate of return on capital. Consequently, Chinese FDI has increased in attractiveness and volume.

European FDI in China has declined in recent years. European players have complained of the many obstacles faced in the Chinese environment, notably poor investor protection, highly uneven and sometimes arbitrarymarket access(EuropeanUnion Chamber of Commerce in China 2019). A key concern has been joint venture requirements in many sectors. These have often involved transfers of intellectual property to Chinese counterparts, reducing the attractiveness of investing in Chinese operations.

China’s presence in the group of major global investors has also created distinct concerns linked to its statedriven economic model. This model can create an unequal level playing field. Against this backdrop, concluding an EU-China bilateral investment treaty would be an important step to regulate cross-border investment between the two economies. The main obstacles on the EU side are the necessary reciprocity for EU companies operating in China, and ensuring that Chinese companies operating in the EU comply with existing rules and regulations and are not favoured by the Chinese government. This is especially the case for state-owned enterprises (SOEs) but could also apply to private companies (García Herrero and Xu, 2017).

Chinese companies have become major competitors of European companies as they top the Fortune 500 list, together with American companies. Furthermore, many Chinese large companies are state-owned, which poses different challenges than competing with American companies, in terms of differing governance levels and financial support. The fact that Chinese companies nowoperate in high value added markets —increasingly doing so in European companies’ areas of strength —combined with the strong role of the Chinese state, has served to heighten European concerns about Chinese investment in EU markets.

Competition between European and Chinese companies does not only affect the Chinese and EU markets. It is also relevant in third markets. As China has become a keyglobal actor and leading technological power, there is a generalunderstanding in the EU that China could assume greater responsibilities for upholding the rules-based international order, as well as greater reciprocity, non-discrimination, and openness of its system. The paper ‘EU-China — A strategic outlook’ makes it very clear that these principles should also be applied to the bilateral economic relationship.

With negotiations on a bilateral Comprehensive Investment Agreement (CIA) underway, our study describes and analyses the EU-China bilateral trade and investment relationship and also assesses which measures to ensure competitive neutrality — a concept advanced by the Chinese —should be prioritised to ensure non-discrimination against EU businesses trading with and/or investing in China. The concept of competitive neutralityaims at measuring the degree of preferential treatment of SOEs. We conclude, based on our own measurement, that SOEs are indeed treated in a preferential manner in China, in terms of a lower effective tax rate and lower interest payments for the same amount of debt.

The Belt and Road Initiative (BRI) is crucially important for China, but also for Europe because the landmass part of the project covers Eurasia and includes as many as 13 EU countries plus a good part of the EU’s neighbourhood. The BRI originally focused on building transport infrastructure but has transitioned towards building soft power for China. It goes without saying that enhanced connectivity can help China strengthen its trade relationships with neighbouring regions, including with the EU. This should create trade gains for EU countries if China does not undermine those gains by creating a free trade area for countries covered by the BRI while excluding the EU, which could even lead to trade diversion away from the EU (García Herrero and Xu, 2016; García Herrero and Xu, 2019).

A key worry about the BRI is that it could lead to debt traps. Public debt levels of BRI countries can be ranked by their (potential) debt to China. Countries including Djibouti (debt to China 69.5 % of GDP), the Kyrgyz Republic (22.6%), Laos (26.3%) and Mongolia (27.8%) are already heavily indebted to China. If all planned BRI projects are realised with the help of additional debt guaranteed by the state, these rates would increase even further: to 154.2% for Djibouti, 92.3% for the Kyrgyz Republic, 60.7% for Laos and 50 % for Mongolia.

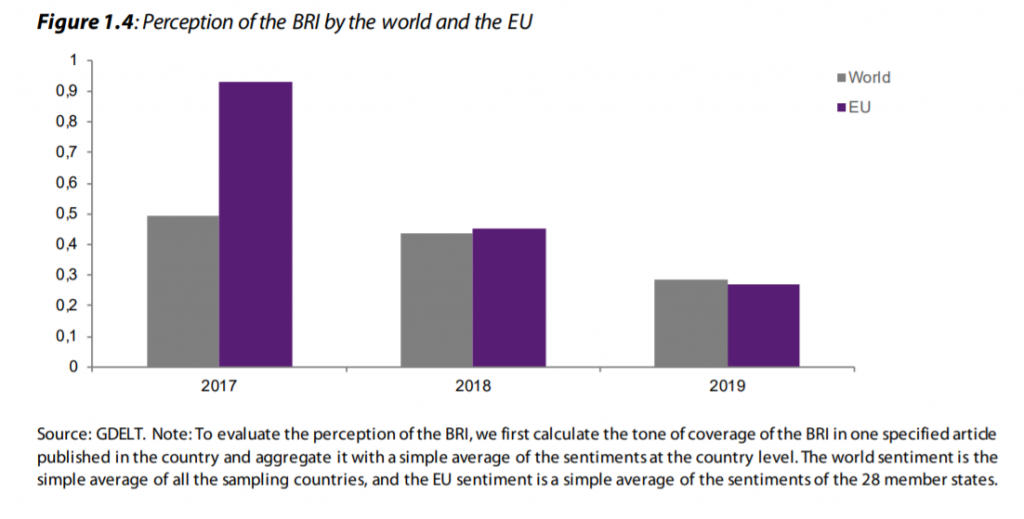

People in EU countries and elsewhere previously regarded the BRI quite positively, but this view has deteriorated rapidly since the first BRI Summit held in Beijing in 2017 (Figure 1.4). To ease global concerns about the BRI, increasingly considered more favourable for China than for others (hub and spoke model), China has pushed towards a more multilateral mechanism, relying more strongly on the Asian Infrastructure Investment Bank. Nonetheless, the general reaction to China’s evolving model is still governed by doubt and, to some extent, by mistrust. China’s push to create a forum of 17 central and eastern European countries interacting with China(known as 17 + 1),rather than enhancing the discussion with EU institutions, does not help. This should be an important point of discussion for any high-level economic dialogue with EU institutions.

When exploring how EU-China relations are likely to develop, China’s social credit system (SCS), to be launched during 2020, needs a closer look. The SCS is considered by the Chinese government as an essential foundation of a modern ‘credit’-based mechanism to monitor and control the market (State Council of China, 2019). But there are good reasons to be deeply concerned about the SCS. Its transparency is likely to be limited, making it difficult to assess possible discrimination against foreign companies. Other major concerns include that privacy might not be respected and the separation of private and business interests might be blurred. Overall, the system could make it harder for EU companies to do business in China. On cybersecurity, China’s new cybersecurity rules (implemented at the end of 2019) allow the Ministry of Public Security to access all the information, data and communications stored on networks of foreign companies operating in China, with major consequences for foreign companies operating in China, including European companies.

In summary, it is in the EU’s interest to foster a positive relationship with China, with a shared objective of advancing bilateral trade and investment, but also to collaborate on global reform in areas such as climate change or the multilateral system. But the EU cannot be naïve. China’s economic system is driven by a highly-invasive state. This creates multiple tensions and complications in the trade and investment relationship. China’s state-driven model also makes fair competition for European companies more difficult. This creates concerns about the level playing field, not only on the Chinese and the EU markets but also on third markets where Chinese and European companies compete. Finally, a powerful Communist Party is also a major political concern for Europe. China is therefore rightly considered not only a partner and competitor but also a systemic rival.

The EU’s attempt to preserve multilateralism and China’s obvious economic importance should serve as a reminder that the pursuit of fruitful and balanced co-existence is the only solution for EU-China economic relations. This means that the EU should have its own China strategy, independent from the US (Leonard et al, 2019). In addition, EU countries should be as united as possible on EU-China economic relations so the negotiating power of the EU is not diluted (García Herrero, 2019). And investment relations are now vital for EU-China economic relations. A well-crafted bilateral investment agreement is of paramount importance for a stable and fair relationship.