When using, citing, or distributing the materials from this report, it is mandatory to reference the ERAI portal and include the webpage address https://index1520.com as the source of information.

China-Europe logistics market

Demand outlook

-

On February 22, US President Donald Trump raised the universal tariff announced the previous day from 10% to 15% for all foreign trading partners [CNBC]. The decision followed a US Supreme Court ruling that overturned most of his sectoral duties (excluding tariffs on cars, auto components, and semiconductors). The repeal of most previous duties lowers the overall rate for Chinese goods. The chaotic nature of US policy could create a window of opportunity for importers and once again lead to a redistribution of international cargo flows. Increased volatility in logistics markets is possible.

-

In January, export conditions for German industry improved slightly. The HCOB Germany PMI Export Conditions Index rose to 51.2 (+0,3 p. MoM) [S&P Global]. The key driver remains sustained demand from Asia (China, Japan, and India). This trend is likely to be sustainable, which could help reduce the trade imbalance between China and Europe.

-

In January, China-Europe-China rail container volume increased by 22% YoY. Giving a breakdown, growth on the Central Eurasian Corridor reached 25% YoY, while the Middle Corridor also showed positive dynamic — 7% YoY. Compared to December, total container volume rose by 8% MoM.

-

Demand for Asia-Europe sea freight is at a reduced level due to the holidays in China. The market remains highly sensitive to changes in the external environment.

Freight rate trends

-

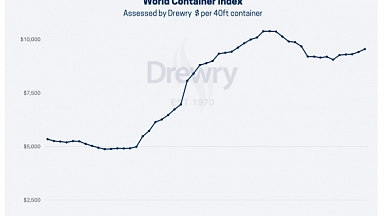

The Shanghai-Rotterdam WCI, as of 19.02.2026, fell to $2 164/FEU (-16% MoM, -19% YoY) [Drewry]. he Shanghai-Genoa WCI dropped to $2 895/FEU. In March, most carriers will attempt to establish a higher price level ahead of Q2 2026 contract negotiations. According to GeekYum, the average spot rate for March starts at $2 700/FEU. However, a significant spread in quotations is observed: from $1 950/FEU (Maersk; ETD 05.03.2026) to >$3 000/FEU (EMC, HMM, ONE, OOCL; various ETD dates throughout the month).

-

Futures traders expect Asia-Northern Europe ocean freight rates to remain in the $1 500-2 200/FEU corridor for the remainder of 2026.

Other trends

-

KTZ Express has organized a pilot shipment of Kazakhstani rice to Antwerp via the Trans-Caspian International Transport Route (Middle Corridor) [rail-news.kz]. The cargo was dispatched along the route Kyzylorda—Aktau—Poti—Antwerp. The Poti-Antwerp sea leg is provided by CMA CGM. Previously, the cargo traveled by land via Semiglavy Mar, Brest, and Duisburg. According to the source, the new scheme has reduced transportation costs compared to the «Northern Corridor» while ensuring comparable delivery times (~30 days). According to ERAI data, in January 2026, the total transit time via the Central Eurasian Corridor on major China-Europe routes was approximately 21 days.

-

Kazakhstan is accelerating the modernization of its railway infrastructure to increase transit between China and Europe. In 2026, it plans to complete the construction of two lines totaling 475 km and modernize 2,900 km of track [Xinhua]. This is expected to increase transit volumes by 60% and reduce delivery time from the Chinese border to the Caspian Sea from 84 to 55 hours.

Ocean freight: the market is entering a phase of seasonal cooling, with a risk of further deterioration in the supply—demand balance

Current Situation and Near-Term Outlook: The seasonal lull has begun. The market remains highly sensitive to changes in the external environment.

-

Demand for Asia-Europe shipments is at a reduced level due to the holidays in China.

-

Significant delays persist in Asian and European ports. According to Flexport, Asian transit hubs are congested due to the accumulation of volumes shipped before the holidays, with terminal utilization exceeding 90%. In Northern Europe, the situation is complicated by adverse weather conditions. In Rotterdam and Hamburg, container yard occupancy is above 85%, and container dwell time reaches 7-10 days. As of 19.02.2026, delays amounted to: 342 thousand TEU in Northern Europe (+7% MoM) and 1.4 million TEU in North Asia (+32% MoM) [Linerlytica].

-

Significant supply adjustments (~40% of weekly capacity, according to Flexport), disruptions in Northern European ports, and equipment shortages in China are constraining supply volumes, which is preventing spot rates from collapsing.

-

The Shanghai-Rotterdam WCI, as of 19.02.2026, fell to $2 109/FEU (-16% MoM, -19% YoY) [Drewry]. The Shanghai-Genoa WCI dropped to $2 895/FEU. In March, most carriers will attempt to establish a higher price level ahead of Q2 2026 contract negotiations. According to GeekYum, the average spot rate for March starts at $2 700/FEU. However, a significant spread in quotations is observed: from $1 950/FEU (Maersk; ETD 05.03.2026) to >$3 000/FEU (EMC, HMM, ONE, OOCL; various ETD dates throughout the month).

Medium- and Long-Term Outlook: The overall trend continues to point towards a growing supply-demand imbalance and intensifying competition.

- According to forecasts (Slide 7), in 2026, spot rates could decline by up to 25%, and contract rates by 10%.

China-EAEU logistics market

Import and export trends

-

In February 13, 2026, the Bank of Russia reduced its key rate to 15.5% per annum against the backdrop of a slowdown in sustainable inflation to 4–5% and the economy’s return to balanced growth. The decision was made taking into account the temporary acceleration of prices in January due to one-off factors (the VAT and excise duty increase, and tariff indexation), which did not alter underlying inflation indicators. Moderate easing of monetary conditions will help stabilize consumer demand and import operations; however, the continued tight monetary policy in 2026 will continue to exert a restraining influence on the dynamics of foreign trade transportation.

-

Starting July 1, 2026, Russia is introducing a Goods Expectation Confirmation System (known by its Russian acronym SPOT), requiring importers to pay VAT in advance before goods cross the border [Kommersant]. This creates an additional fiscal burden for businesses and aims to combat gray schemes for importing goods from EAEU countries. Since February 21, Kazakhstan has tightened requirements for electronic advance notification for international road carriers: detailed data on the cargo, participants, and scanned documents must now be provided [RZD-Partner]. Both changes form a unified trend towards digitalization and tighter control within the EAEU, while Kazakhstan’s innovations directly affect only road transport, whereas Russia’s SPOT system applies to all modes of transport when importing from union countries.

-

The Russian Government has approved a draft agreement with China on the joint construction of a second main track using Chinese standard gauge (1435 mm) on the cross-border section of the Zabaikalsk — Manzhouli railway [Prime].

-

According to a Rosatom forecast, cargo transportation volumes along the Northern Sea Route (NSR) will approximately double in 2026 [Vesti]. Following a pilot project in Chukotka, five more Far Eastern regions will join the program, allowing volumes to increase from 160 thousand tons in 2025 to more than 300 thousand tons in 2026.

-

PBC Container Index rose to $6 656/FEU in mid-February 2026 (+3% MoM). The increase was primarily driven by rising rates for direct container trains from China to Russia. Tariffs increased by an average of $300/FEU (+6% MoM) due to a shortage of space on rail services, as well as mass delays in train departures from Chinese stations. At the same time, ocean freight rates from China to Russia’s eastern, western, and southern ports showed weak dynamics in February.

Other trends

-

The capacity of the Altynkol — Khorgos railway junction on the Kazakhstan-China border is planned to be nearly doubled — from 18 to 33 train pairs per day [Forbes]. This will become possible thanks to the construction of second tracks on the Altynkol — Zhetygen section and the development of sidings; work is planned to be completed in 2026.

-

KTZ plans to conduct an IPO of at least $1 billion in May. According to Bloomberg, KTZ is exploring the possibility of a dual listing: on an exchange in Kazakhstan and abroad. It plans to place up to 25% of its shares.