When using, citing, or distributing the materials from this report, it is mandatory to reference the ERAI portal and include the webpage address https://index1520.com as the source of information.

China-Europe Logistics Market

Demand outlook

- China’s exports to the EU rose 9.2% YoY in July, as trade reorientation and resilient demand for Chinese goods continued to support cargo flows to the bloc. Imports from the EU, by contrast, fell 1.6%, reflecting subdued domestic demand in China. Both manufacturing PMIs (Caixin and NBS) unexpectedly dropped below the neutral 50 mark, with a significant drag from declining orders, including export ones [NBS, Trading Economics]. In the absence of new stimulus measures, manufacturing and shipment growth may slow, marking the imminent end of the peak season.

- July PMI data point to a modest improvement in the eurozone: manufacturing PMI rose to 49.8 — a 3-year high — yet export orders fell after a brief stabilization, posting the sharpest drop in four months [S&P Global]. Despite output growth and recoveries in select countries, external demand remains weak. By sector, new business growth was recorded in banking, transport, and tech equipment, while chemicals and pharmaceuticals saw steep declines [S&P Global]. Given the weakness in international demand, the EU’s export momentum remains constrained.

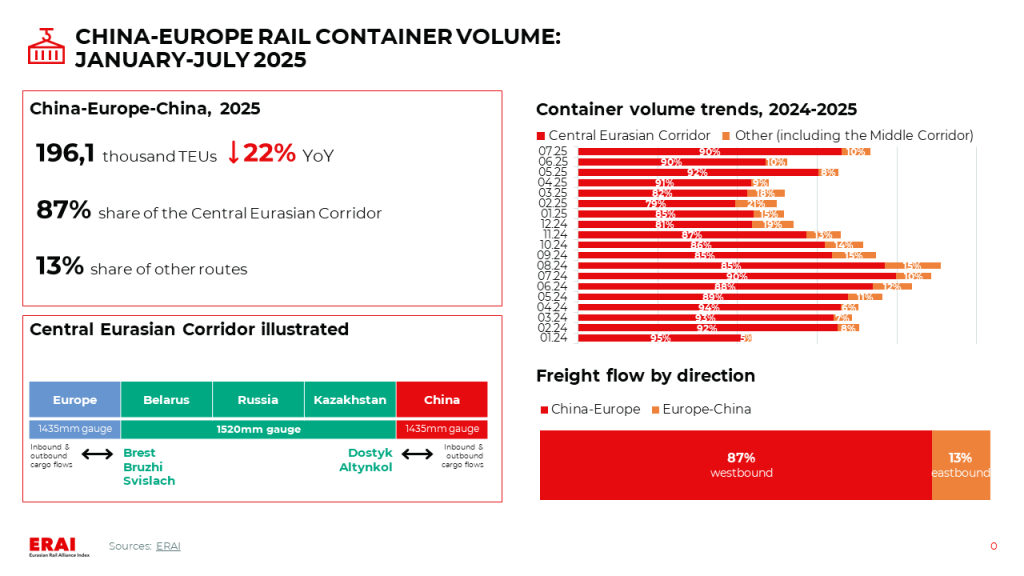

- For January—July, China—Europe—China rail container volumes fell 22% YoY. In July alone, total volumes across all competing routes declined 17% YoY but rose 40% MoM, driven primarily by gains in the central Eurasian corridor.

- As the traditional peak season winds down, demand for ocean freight from Asia to Europe is softening [Flexport]. Nevertheless, market balance remains intact in the near term. Some cargo remains unshipped, keeping vessel load factors high.

Freight rate trends

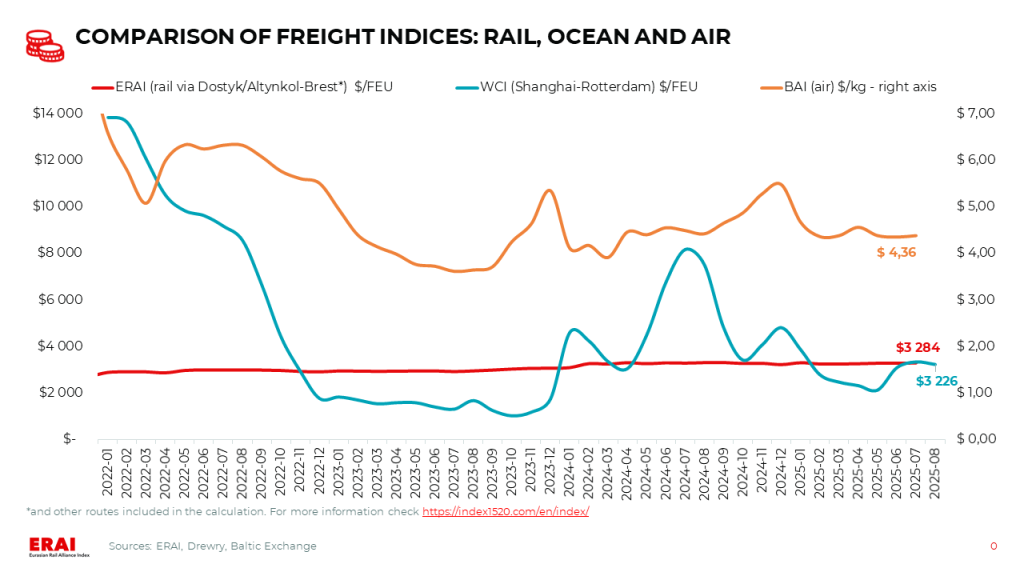

- The WCI Shanghai—Rotterdam rate was broadly unchanged last week at $3 276/FEU (-3% MoM, −59% YoY) [Drewry]. After peaking in early July, rates have been edging lower. For August, Linerlytica reports carrier guidance in the ~$2 500–2 900/FEU range. GeekYum data indicate ~$2 700–3 100, with widening pricing divergence: COSCO is holding above $4 000, while Maersk has offered $2 270 for late August. Hapag-Lloyd (Maersk’s Gemini Cooperation partner) has already announced its September rate — around $2 800/FEU. Port delays in Asia and Europe are, for now, preventing a sharper market decline.

UPDATE: As of the evening of August 14, 2025, the latest WCI Shanghai-Rotterdam reading has declined by 3% WoW — down to $3 176/FEU.

- Futures pricing, based on contracts published by the Shanghai Futures Exchange, points to a rate drop in H2, with a marked trough in September—October. The forward curve implies a decline on the Asia—Europe lane from current levels to around $2 700/FEU by end-August, and to ~$1 800/FEU by end-October.

Other trends

- China Railway Container Transport (CRCT) has joined Middle Corridor Multimodal Ltd. [Interfax], a joint venture established in 2023 by the railways of Azerbaijan, Georgia, and Kazakhstan. The decision was taken at an extraordinary general meeting in early August, following discussions ongoing since at least mid-2024 [Interfax].

- A new terminal will be built in Małaszewicze, developed by Container Terminal Mala (CLIP Group) in partnership with TorKol [Railway Supply]. The facility will handle transshipment between 1 520 mm and 1 435 mm gauges, as well as between rail and road transport. The project includes new track infrastructure, upgrades to existing lines, modern transshipment equipment, and IT systems. Completion is scheduled for June 2026.

|

|

Ocean Freight: a Fragile Market Equilibrium

Current Situation and Near-Term Outlook: rates are likely to remain under downward pressure, particularly given the fading seasonal momentum and the absence of new supportive factors.

- As the traditional peak season winds down, demand for ocean freight from Asia to Europe is softening [Flexport]. Nevertheless, market balance remains intact in the near term. Some cargo remains unshipped, keeping vessel load factors high.

- The WCI Shanghai—Rotterdam rate was broadly unchanged last week at $3 276/FEU (-3% MoM, −59% YoY) [Drewry]. After peaking in early July, rates have been edging lower. For August, Linerlytica reports carrier guidance in the ~$2 500–2 900/FEU range. GeekYum data indicate ~$2 700–3 100, with widening pricing divergence: COSCO is holding above $4 000, while Maersk has offered $2 270 for late August. Hapag-Lloyd (Maersk’s Gemini Cooperation partner) has already announced its September rate — around $2 800/FEU. Port delays in Asia and Europe are, for now, preventing a sharper decline.

- Significant delays persist at major hubs in Asia and Europe. As of 10 Aug 2025, disruptions affect 1.4 million TEU in North Asia (including China, +10% MoM) and 285 000 TEU in Northern Europe (-15% MoM) [Linerlytica]. In Asia, conditions are further complicated by the typhoon season, which will last through October and continue to disrupt port operations [Kuehne+Nagel]. In Europe, additional constraints stem from maintenance works and limited rail infrastructure capacity, particularly in areas adjacent to ports.

Mid-and Long-Term Outlook: the overall trend, as before, points to a growing imbalance between supply and demand and intensifying competition among carriers.

- Drewry forecasts a return to a downward trend in the second half of 2025, with weakening demand and falling freight rates.

China-EAEU Logistics Market

- According to Autostat, 120.6 thousand new passenger cars were sold in Russia in July 2025 (-11.4% YoY), and 651 thousand in January—July (-23.9% YoY). In August, dealer estimates point to sales of 110–130 thousand units. Demand is supported by clearance sales, available inventories, and the Bank of Russia’s key rate cut. Given the substantial share of Chinese vehicles in imports, demand trends have a direct impact on logistics between China and Russia.

- In H2 2025, analysts expect a shift in consumer behavior — from inflation-driven impulse buying toward more deliberate big-ticket purchases [Kommersant]. Growth potential is underpinned by savings accumulated under last year’s high interest rates and the subsequent decline in deposit yields. This may support demand for cars, household appliances, and home goods. Retail sales growth is expected to slow to 9.2% in nominal terms (vs. 11% in H1), while total consumption is projected to ease to 11%. Leading indicators point to a notable cooling in economic activity in early 3Q 2025, limiting the scope for faster consumer recovery.

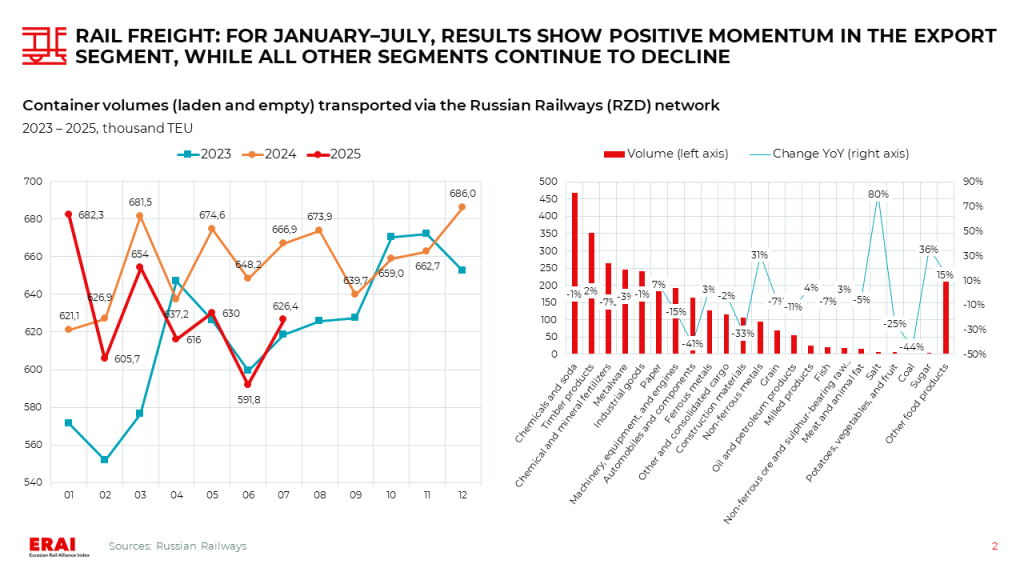

- In January—July 2025, Russian Railways transported 4 406 thousand TEU (laden and empty) across all service types, down 3.3% YoY [RZD]. June volumes totaled 626.4 thousand TEU, up 5.8% MoM. This included 1 740 thousand TEU in domestic traffic (-3.8% YoY) and 1 039 thousand TEU in exports (+8.3% YoY). Laden container volumes across all service types reached 3.1 million TEU (-5.6% YoY).

- The InfraNews Rail Market Confidence Index came in at −11.11 points for late July—early August, up from −14.81 in June, remaining in negative territory and signaling persistent pessimism. While current conditions were assessed slightly more positively, short-term expectations worsened. Market participants anticipate higher loading volumes in August—September on the back of the grain season and lower interest rates — factors that, amid ongoing infrastructure constraints, could further strain the network.

- Import rates in China—Moscow multimodal traffic have inched up over the past month. Following a prolonged decline, the market may be on a recovery trajectory. Average costs via Far Eastern ports are ~$3 700/FEU (SOC) and ~$3 900/FEU (COC), up by ~$100 MoM. Rail rates remain slightly below ~$4 000/FEU (COC), with minimum rail quotes around ~$3 200–3 400/FEU (SOC).

- Kazakhstan Temir Zholy (KTZ) has imposed a ban on moving empty flatcars from all Kazakh rail stations to the interstate junctions of Altynkol—Khorgos and Dostyk—Alashankou on the Chinese border [KTZ]. The restriction will remain in force through 31 August 2025.

Rail Freight: for January—July, Results Show Positive Momentum in the Export Segment, While All Other Segments Continue to Decline

In January—July 2025, Russian Railways (RZD) transported 4 406 thousand TEUs (laden and empty) across all service types, down 3.3% YoY [RZD]. July volumes totaled 626.4 thousand TEUs, up 5.8% MoM.

- This included 1 740 thousand TEU in domestic traffic (-3.8% YoY) and 1 039 thousand TEU in exports (+8.3% YoY). Loaded container volumes across all service types reached 3.1 million TEU (-5.6% YoY).

- By commodity, the removal of export duties and easing of restrictions in Western markets drove a surge in copper shipments from Russia to China in H1 2025— up 81% YoY, exceeding the full-year 2019 level [Kommersant]. The bulk consisted of cathode copper and raw materials (ore and concentrates). Given the sustained recovery in Chinese industrial activity and constrained global supply, there remains potential for further export growth.

|