Copenhagen-based Sea Intelligence said in its weekly analytical report that a global volume loss due to COVID-19 impact has reached 1.9 million TEU amid blanking of sailings by global carriers.

Carriers are blanking sailings as a way of dealing with the cargo volume slump caused by the coronavirus outbreak originating from China and the closure of manufacturing plants in the country as a precautionary measure aimed at curbing the outbreak.

At a rough average freight rate of 1,000 USD/TEU, this equals to a revenue loss of USD 1.9 billion for the carriers.

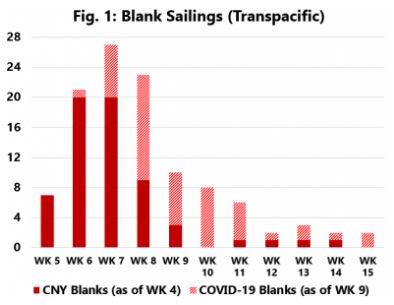

The number of blank sailings in weeks 5-15 of 2020 on the Transpacific has increased to 111, of which 48 have been blanked due to COVID-19, and the remainder due to «normal» Chinese New Year capacity management.

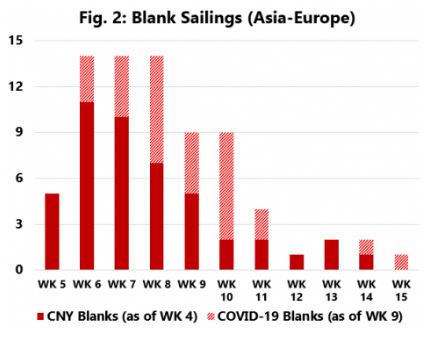

On Asia-Europe, the number of blank sailings has increased to 75, of which 29 are due to COVID-19, the intelligence provider said.

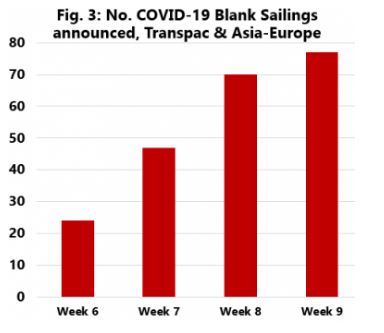

«From a more positive angle, we appear to be seeing a stabilization. Even though the carriers have announced 7 more blank sailings over the past week, which corresponds to an additional 7% removal of capacity, the pace of new blank sailings has clearly declined, suggesting a belief from the carriers that volumes will slowly be brought back to normal levels. The bulk of the blank sailings were announced during weeks 7 and 8,» Alan Murphy, CEO, Sea-Intelligence, said.

«This, however, does not mean the ripple effects are over — far from it. We have already outlined in the past weeks how this will impact the round-trip dynamics and create shortages of both vessel capacity and equipment availability. Carriers are already pushing rate increases on account of this, and for some back-haul shippers the coming weeks might well be a matter of whether they can get their cargo moved at all, almost irrespective of the price they are willing to pay.»

The capacity management measures have ensured freight rates remain on the same levels, for now, staving off a feared financial-crisis-like rate implosion.

Furthermore, there were fears that should the situation get prolonged, that aside from blanking of sailings, carriers would have to resort to heavier capacity reduction measures such as idling of ships and demolitions.

This might not be the case, as there are signs that the cargo flow situation at coastal ports in China is normalizing as manufacturing plants start to reopen.

Graphs: Sea Intelligence